How to Navigate 2026 Headwinds

The news is heavy, and we understand if you’re feeling the weight of it and pressure to change your investment strategy. Between the onset of a war in Iran, escalation in tension and conflict throughout the Middle East, and a cooling labor market where unemployment has ticked up to 4.4%, it is human nature to want to do “something” to protect your account balances.

When the headlines feel alarming, many investors feel pressure to “do something” to protect their portfolios. After making space and time to address this uncertainty, the most important thing I can tell you today is also the least exciting. If built correctly, your financial plan has the capacity to sustain this exact kind of uncertainty.

Acknowledging the Noise

This moment in time is serious. We are witnessing real human tragedy with meaningful geopolitical shifts. Financial markets have responded: volatility has surged and major indices around the world have tested their resilience.

When uncertainty rises, it’s natural to look for forecasts and predictions that let you know what’s next. Many investors want to know:

- When will the conflict de-escalate?

- Is the economy headed to a recession? This is an almost perpetual question in the modern age, even as recessions have become less frequent.

- Should I adjust my investments now?

After more than 25 years in the investment and financial planning profession, I believe in one piece of investment wisdom above all others.

Predictions often cost investors more money than they protect.

Predictions oversimplify complex systems. They are often peddled by someone with something to sell. They lead to the kind of overconfidence and whiplash reactions that create more risk than they solve.

Instead of looking for soothsayers with knowledge of the future, we encourage investors to focus on building strategies that acknowledge that there is uncertainty over time. That’s how we build our clients’ portfolios.

Your Investment Strategy Should Be Built for Uncertainty

Instead of chasing a crystal ball prediction, our approach at Pearl Planning centers on a few core truths:

- Volatility is the Fee, not the Fine: Market dips and downturns are the price of admission for long-term investing success. They aren’t a signal that the system is broken or this time is different, they are a reminder of why we diversify. Volatility is never pleasant, but it is normal. A recent lesson: Last year at this time, we were facing a near-miss on a bear market and epic tariff announcements. Large US companies started the year strong, up 4.6% through mid-February 2025. Then major tariff announcements reversed the momentum and by mid-April, the year-to-date returns were down almost 15% and the market had pulled back by almost 20% from year to date highs. Things felt terrible and pessimism was all around. But the markets rallied as tariff promises diminished and better news in other parts of the economy prevailed. By the end of the year, large company stocks were 17.88% higher than where they had started. It sure didn’t feel like that’s how the year would’ve turned out in March and April.

- Financial Plans are Not Built for Only Sunny Days: Long term market returns seem predictable, but a typical year’s return fluctuates wildly from long-term averages. We built your portfolio knowing that years like this one, marked by conflict and potential economic shifts, would happen. The lessons learned from just the last 12 months are affirming for an approach emphasizing patience and diversification.

- Focus on What You Can Control: We won’t be able to control or the Bureau of Labor Statistics unemployment numbers. We can control your savings rate, your emergency reserves, and the decision to stick with your investment process.

Staying the Course

As an investor, you can’t control geopolitical shifts, inflation data, or unemployment reports. But there are many things that you can control:

- Your savings rate

- Your investment allocation

- Your emergency reserves

- Your tax strategy

- Your long-term investment discipline

A down market or a geopolitical shock doesn’t mean you have to freeze. It means we stick with the mechanics of our investment process: we didn’t wake up this month thinking it’s time to rebalance, we’ve been consistently rebalancing over the last year, ensuring your cash reserves are as intended and keeping your eyes on the horizon.

Our goal for you remains the same: achievable returns over full market cycles, a down-to-earth strategy built for decades, and a connection between your investment process and your financial plan. We are watching the news, aware of the economy and markets, but we aren’t letting this week’s headlines drive the car.

A Picture is Worth a Thousand Words – Putting 2026 into Context

Sometimes a picture is worth a thousand words. Here is some information on what has happened so far this year (as of March 13th).

Investment Performance Year to Date

In spite of the gloomy atmosphere, through March 12th, US large company stock are down only 2.3% on the year. US bonds are clinging to positive returns (up 0.1% year to date) in spite of rising interest rates which have marched higher along with the price of oil. International investments have fared better having had a very good start to the year. Meanwhile, the prices of commodities (including oil) and gold have surged.

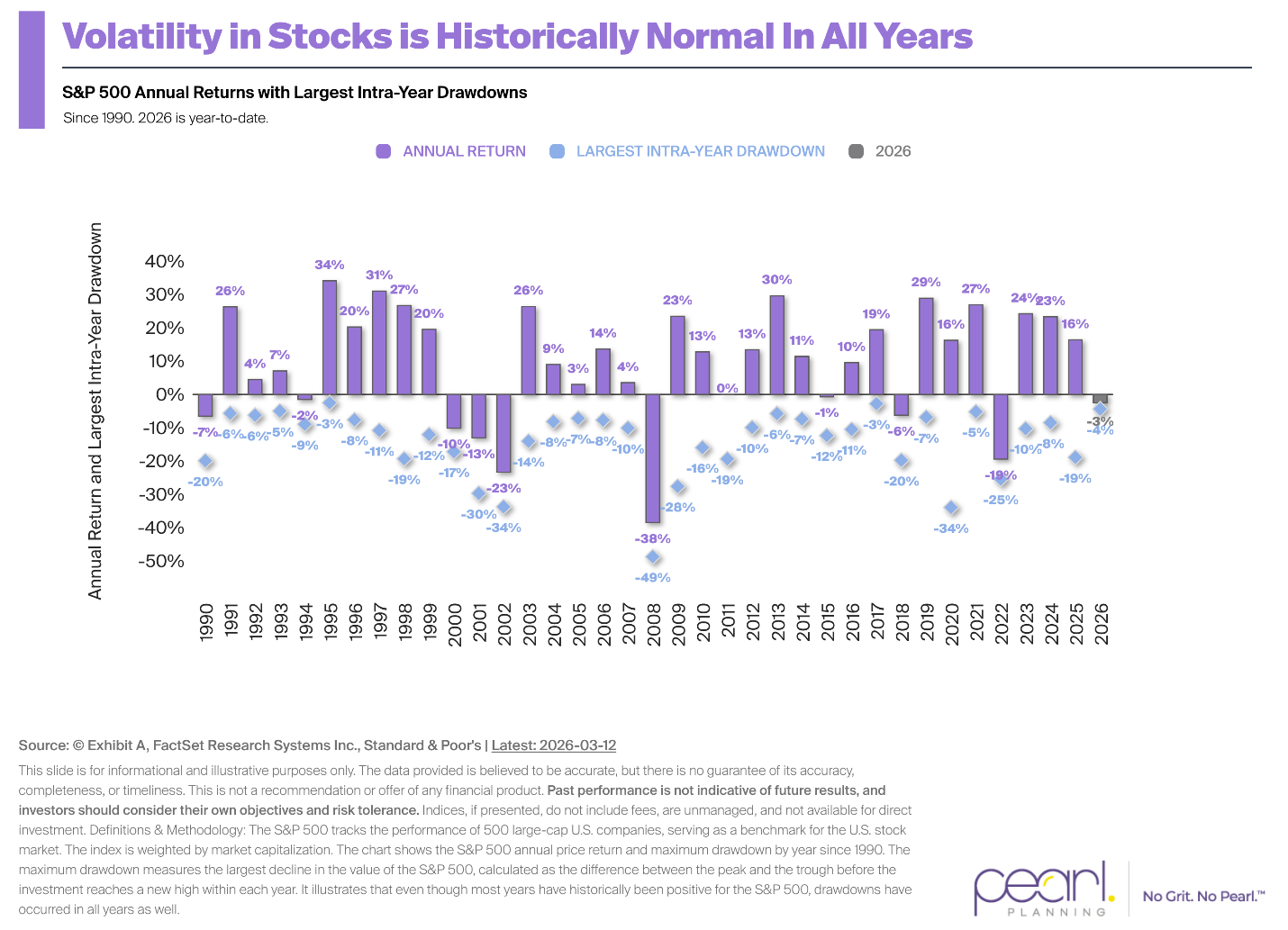

Intrayear Market Declines are Typical

Looking back over time, it is typical to have intra-year market drawdowns. When you look back to 1990, the current pullback of 4% as of 3/12/2026 is below average for full calendar years.

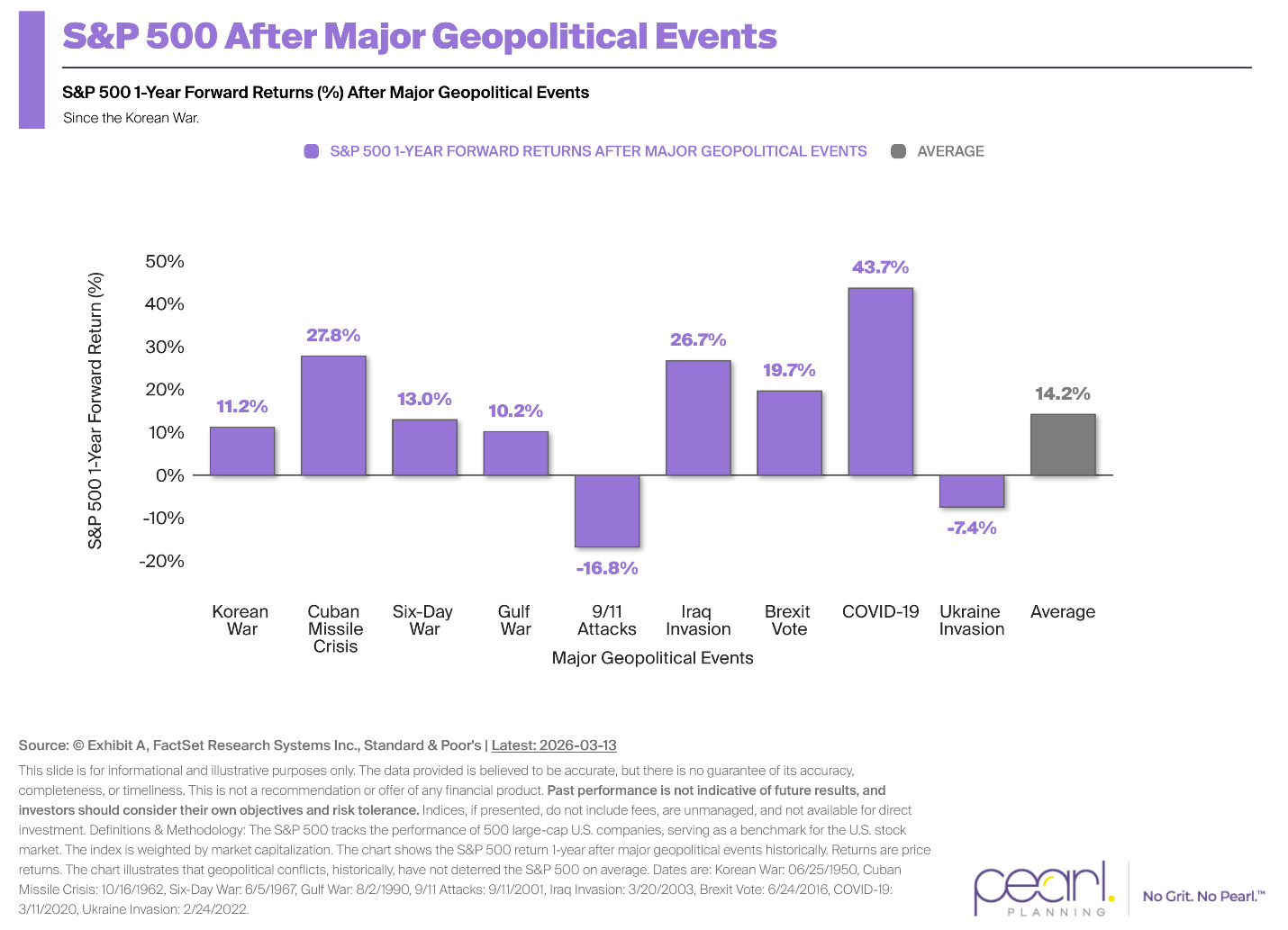

Geopolitical Events & Forthcoming Market Returns

Stock markets do not always bow to war and geopolitical events. Here’s a look at past wars and other major events in history back to the 1950’s and stock market returns for the following 12-month period.

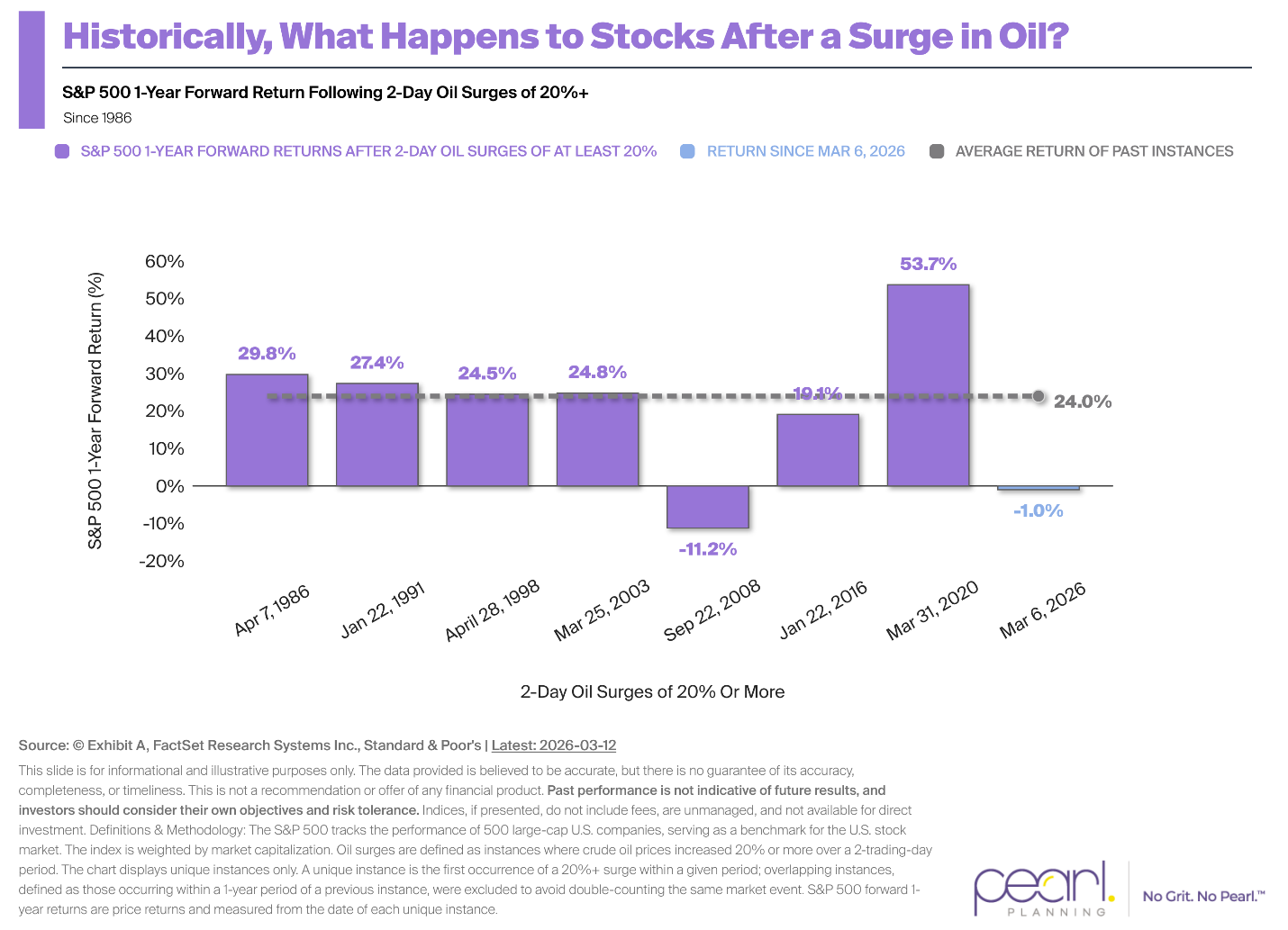

Oil Surges Aren’t Always Crushing for Stocks

In the past, oil price surges have often been followed by positive stock market returns in the following 12 months.

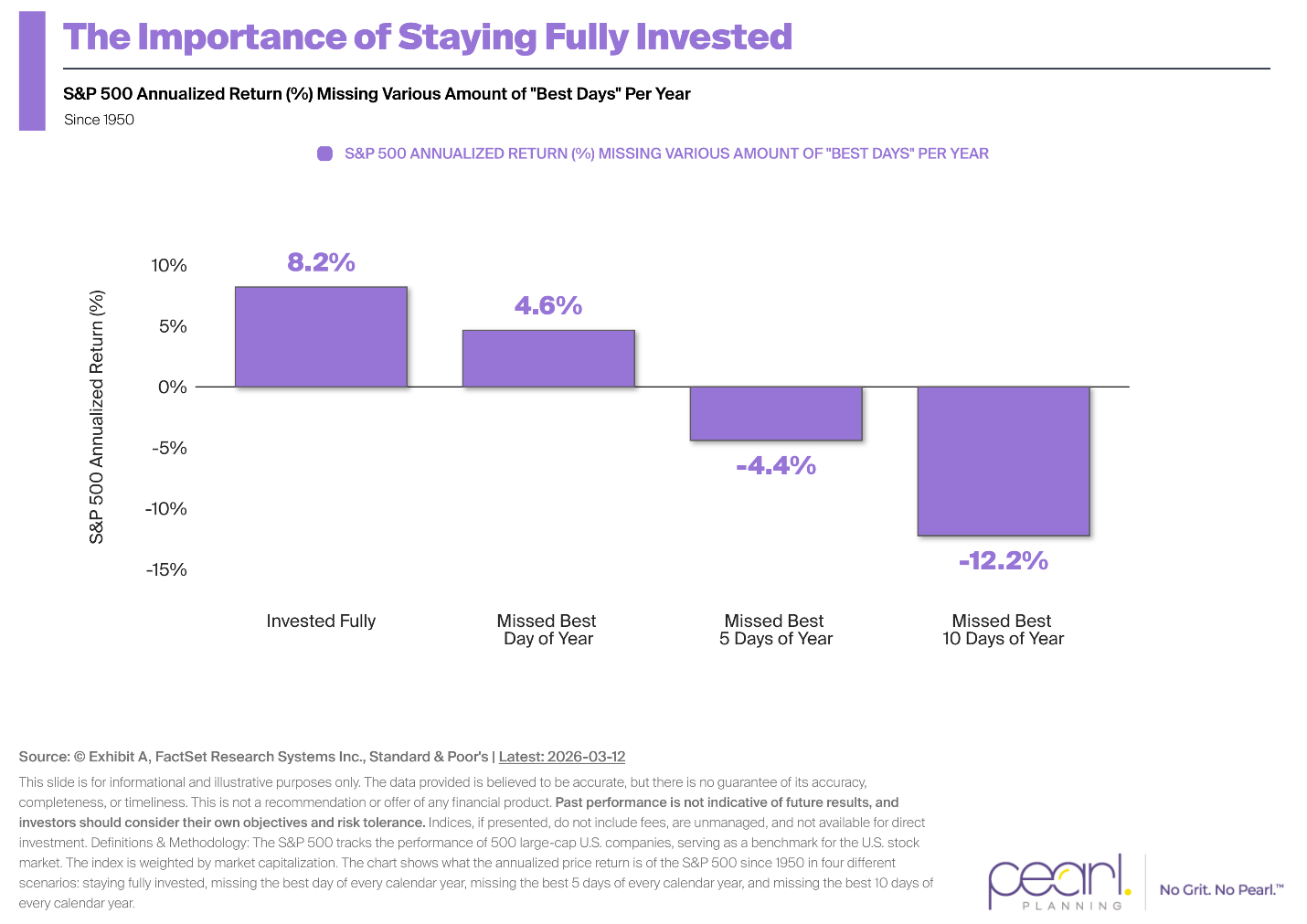

It’s Important to Stay Invested

It can feel safer to step away from markets when the news is overwhelming. Unfortunately, even minor moves away from your investments can have long-term impacts. Here’s a look at market returns if you missed the best performing day of the year or more. Unfortunately, the best days often cluster with the worst days.

What Can You Do in Uncertain Times?

If uncertainty makes you feel like you should take action, focus your energy on moves that strengthen your financial foundation rather than reacting to short-term market movements.

Consider these steps:

Start With Your Investment Strategy

If you already have an investment strategy designed for “all-weather” conditions, one that is diversified and aligned with your long-term goals, the most productive action may simply be to stay the course.

However, market stress can also reveal weaknesses in a portfolio. If you’re realizing that you don’t have a clear investment strategy, or that your portfolio feels far riskier than you’re comfortable with, this may be the right time to step back and revisit your investment process. A thoughtful investment process and discipline should give you confidence in both strong markets and difficult ones.

Stress-Test Your Liquidity

Ensure you have an emergency fund covering 3–6 months of essential expenses in cash or a high-yield savings account. Retirees may want to maintain up to a year of cash-like reserves to avoid selling investments during a downturn.

Harvest Tax Losses

Market declines can create opportunities for tax-loss harvesting, allowing investors to offset future capital gains.

Rebalance Your Portfolio

If market movements have shifted your stock-to-bond allocation, rebalancing can help maintain your intended risk level.

Keep Automatic Investments Running

For investors still saving for retirement, market dips mean new contributions are buying investments at lower prices, an important advantage of long-term investing.

Revisit Your Financial Plan

In times of economic uncertainty or rising energy costs, reviewing discretionary spending can help create additional financial flexibility.

The Bottom Line

Periods of uncertainty are uncomfortable, but they are also a normal part of investing.

At Pearl Planning, we believe successful investors are not those who avoid volatility, but those who plan for it, prepare for it, and stay disciplined through it.

A thoughtful financial plan connects your investments to your real-life goals including retirement, career flexibility, supporting family, and living the life you want. When those pieces are aligned, it becomes much easier to stay steady when markets and headlines feel chaotic.

If you already have a clear strategy built for long-term investing, the best move may simply be to stay the course. But if recent market volatility has you questioning whether your portfolio is truly aligned with your goals, or if you’re realizing you’ve never had a coordinated investment strategy and financial plan in the first place, it may be time to take a fresh look at your financial plan.

At Pearl Planning, we help individuals and families build investment strategies that are designed to weather uncertainty and support their long-term financial lives.